NTUC Income’s Organizational Reform, Marketing, and Digitalization

Kanae Fujii

Public Relations

ZENROSAI

In November 2016, I participated in the High Potential Course (HPC), one of the Leadership+ programs of ICMIF held in Singapore and hosted by NTUC Income of Singapore. As part of the HPC curriculum, I had the opportunity to visit the headquarters and a branch of NTUC Income on the first day of the program and to receive a briefing. What I learned from the visit and briefing was so interesting and left such a strong impression on me that I decided to summarize it in a report to share with you.

In November 2016, I participated in the High Potential Course (HPC), one of the Leadership+ programs of ICMIF held in Singapore and hosted by NTUC Income of Singapore. As part of the HPC curriculum, I had the opportunity to visit the headquarters and a branch of NTUC Income on the first day of the program and to receive a briefing. What I learned from the visit and briefing was so interesting and left such a strong impression on me that I decided to summarize it in a report to share with you.

For those of you who are not familiar with NTUC Income, it is a trade-union-affiliated insurance cooperative that has always been a leader holding a large share in the Singaporean market. Singapore’s insurance market became a target for foreign insurance companies as the country experienced economic growth, prompting NTUC Income to conclude that it needs not only to be evaluated based on the value of trust as it has been, but to also be strong and dynamic to match the times. Through “the Cultural Revolution” (1,500 days starting in August 2007)—a reform meant to improve the quality of the organization while maintaining a balance between the principles of a traditional trade union and the essential qualities of an insurance company—NTUC Income changed its corporate culture from one that became more inward-looking as the organization grew into a more professional organization.

The organization was reformed further by conducting in rapid succession “the Orange Revolution” (1,500 days from September 2011), which aimed to differentiate the Cooperative from others by rebranding products to cast off the old brand image and appeal to young consumers. This history shows that this cooperative is an extremely action-based organization.

“The Digital Revolution” currently underway is meant to allow the Cooperative to keep pace with the changing actions of consumers by introducing various technologies in products and services, while implementing new ideas by working with such young companies as start-ups.

Many participants of the AOA Seminar held in Tokyo on Oct. 25, 2016 clearly remember the words of NTUC Income CEO Ken Ng. He said: “We mutual-aid groups need to keep pace with the changing actions of consumers, and digitization will change insurance and mutual aid. We cannot be left behind by this change, so conducting reforms to keep up with change is the secret for us mutual-aid groups to survive and succeed.”

Ⅰ.Recent Efforts Conducted by NTUC Income

- Date and Time: Monday, Nov. 7, 2016, from 2:00 p.m. to 3:00 p.m.

- Location: NTUC Income headquarters

- Speakers:

Chief Executive Officer Ken Ng (10 years at the Cooperative) Chief Marketing Officer Marcus Chew (2 years at the Cooperative) - Participants: 7 participants of HPC, and Steve Barry (Training Instructor, Origos Consultancy)

- Outline:

Mr. Ken Ng gave a presentation titled “Organization Change and Digital Innovation.” Then Mr. Chew provided supplementary explanation, and this was followed by a Q&A session. The following is a summary.

(1) About the Cultural Revolution

1) Internal Reform

- This is the first revolution conducted by new management team. In Singapore, which has Chinese roots, the use of the term “Cultural Revolution” was a way to show the importance of the undertaking.

- Reforming the organization is more difficult and takes time compared to an external reform, such as that of brand image. In fact, 10 years have passed since the start of the Cultural Revolution and the subsequent Orange Revolution, but internal reform is still not finished.

- By upgrading the “outer frame” and “perception from the outside,” through such steps as rebranding and digitization, we have created internal pressure to change in order to align the external change.

2) Internal Reform and Leadership

- Compared to a stock company whose results are evaluated quarterly, a social enterprise is able to have a long-term viewpoint but its vision and direction tend to become vague.

- The role of management is to minimize ambiguities and provide concrete common understandings among employees so that each person can perform his or her role.

- The management team clarified each item, such as “basic values,” “required specialization,” and “approach when dealing with clients.”

[Example]: The employees did not have a common understanding of “what a social enterprise is.” The claim handlers mistakenly believed that the role of a social enterprise is “to sympathize with the policyholder and make a judgment that benefits the policyholder the most.”

→ The necessary value was clarified as “fairness,” not “compassion,” and every staff was asked to improve the quality of business to the same level.

3) Securing and Training Personnel

- A large number of personnel were replaced as well as part of internal reform.

- With the exception of the current CEO, Mr. Ken Ng, the entire management team has left over the past 10 years.

- At the employee level, the past 10 years has mostly been about securing personnel from the outside rather than cultivating personnel internally. The cultivation of personnel internally is an issue for the future.

- A management training program has been offered the last five years ago in order to cultivate and utilize young personnel. Leader teams have been created to experience management, but promoting them is not easy because they need to produce results in their work.

- Specialization and necessary skills are different depending on the department, so age groups are also different. The core departments in the insurance business consist of a large number of experienced workers. On the other hand, the marketing team is young; many are 28-30 years old, with the average age in the mid-30s.

(2) About the Orange Revolution

1) Brand Logo

- The new logo was considered over about two years. In addition to the color change, the current design does not include the word NTUC but instead has the NTUC logo at the front in order to weaken the image of their background.

- During this process, there were objections from the inside to the proposed new logo, but they were persuaded by showing them that among the proposed designs, the current design will be preferred by more people based on neuroscience.

- The “made different” phrase in the logo shows that NTUC Income has a different structure than stock companies and others, which is the basis for how the organization differentiates itself.

![]()

2) Unification of Brand Recognition

- Since insurance is a financial service that cannot be seen, the color was used as a unified image in order to boost visibility.

- For example, “Orange Force” (a service in which an accident response team riding orange motorcycles rushes to the scene of an accident involving an automobile insurance policyholder) is part of the strategy to make NTUC Income’s services visible among customers and the public, which create a better recognition of the brand.

3) Advertising

- To establish a new brand image, advertising was completely overhauled to make it well-received by young people.

- Initially, there was concern that existing policyholders would be dissatisfied. But in order to revamp the image, the old and new ways were not used simultaneously.

- As a result, the new image of the brand became clear. And existing policyholders—the parents of the targets of the advertisements—said that the advertisements help in getting their children to understand insurance.

- We will not promote that we are a Cooperative. The “we are a Cooperative” appeal is based on a self-centered way of thinking. When putting the customer first, it would be fine if they feel that we are Cooperative-ish through our services.

- We are conducting aggressive advertising, with a willingness to take risks. Although we are constantly discussing what the acceptable limits are, we are aiming right at the borderline. As such, we are closely watching reactions on SNS.

[Example]: In an effort to encourage young people to start retirement planning, we conducted a major campaign to start Retiring instead of waiting for Retirement. We had an actress say that she is retiring, but this led to rumors that she is retiring from show business, resulting in a firestorm on SNS. At the request of TV stations, we placed ads on national newspapers for seven consecutive days to explain that the retiring comment was part of our campaign. (However, we did not apologize because there was nothing wrong with our effort and there were no errors.)

(3) About the Digital Revolution

1) About the Use of Digital Technologies

- Provide what is wanted, based on the understanding that consumer decides the service.

- Since people are increasingly communicating via digital tools, the method of communication between customers and the insurance cooperative should be also being updated.

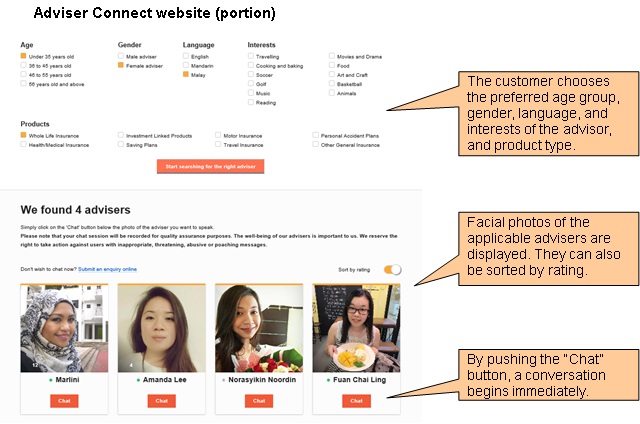

2) Adviser Connect (online matching with an adviser)

- This is a service in which the customer can choose the advisor to receive insurance consultation via online chat.

- No difficult technologies are involved. We just changed our way of thinking to: The customer has the right to decide.

- The skill required of advisers is, during a chat averaging 5-10 minutes, to bring the communication to the next stage, which is telephone or face-to-face meetings. Advisers are currently acquiring those skills, such as timely communication through text and closing skills.

- Now that two years have passed since operations began, we plan to analyze the data, such as ascertaining trends of advisers that are preferred by customers.

Ⅱ.Tour of NTUC Income Branch

- Date and Time: Monday, Nov. 7, 2016, from 3:30 p.m. to 4:30 p.m.

- Location: Bras Basah Branch at NTUC Income Headquarters

- Speaker: Manager of the NTUC Income Bras Basah Branch

- Participants: 7 participants of HPC, and Steve Barry (Training Instructor, Origos Consultancy)

- Outline:

The tour was of the flagship branch, the largest, which is located at headquarters.

(1) About the Development of Branches

Number and Operating Hours of Branches

- 7 stand-alone Branches (of which 2 are adviser locations that have no counter functions) and 5 Lite Branches, such as those inside supermarkets.

- Branches were consolidated and organized during the Orange Revolution to improve efficiency.

- Operating hours are shown below. The peak time differs depending on the location.

Branch Type Business

DaysOpening Time Closing Time Remarks Branches

(stand-alones)Mon.-Fri. 10:00/10:30/11:00 a.m. 6:30/7:00/7:30 p.m. Sat.-Sun. 10:00 a.m. 4:00/4:30 p.m. No weekend service at 1 branch Lite Branches Mon.-Sun. 11:00 a.m. 8:00 p.m.

(2) How the Branches Work

1) At the entrance

- At the entrance, customers scan their National Registration Identity Cards (NRICs) to verify their identity and allow us to collect customer-visit information.

- At the same time, customers choose the reason for their visit from following five options, and they receive a number ticket.

- Customer-visit information from all locations is collected at the Central Back Office (explained later) in real time so that operating rates of locations can be ascertained and managed.

- Based on our research conclusion that “wait time of up to 18 minutes can be endured,” we set a target wait time and around 90% of all branches achieve this.

1) Renewal of car insurance This accounts for about 50% of visitors. 2) Submission of insurance claim 3) Payment of premium 4) Elderly Those who are 65 years old and up receive priority service. 5) Others Very few people come to newly enter a policy, so that option has not been set.

2) At the counter

- Stand-alone branches have the following three types of counters:

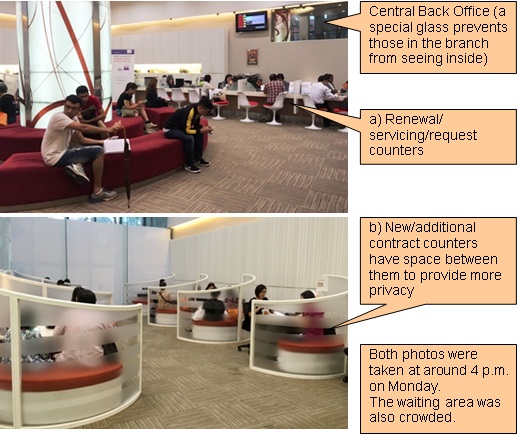

- Renewal/servicing/request counters (8-14 seats): The main counters. After the customer has completed the procedures, a confirmation is made about the contents of servicing requests and whether the customer seeks consultation, and they are directed to the counters in b) below if necessary.

- New/additional contract counters (10-14 seats): Advisers are always stationed here to upsell and cross-sell to new policyholders as well as those who came to the location for other reasons. Procedures are kept separate from insurance consultation and contract signing to prevent cases in which customers were just conducting procedures but while doing so, they were persuaded to buy and signed a contract before they knew it.

- Payment counters (3-5 seats): By law, financial institutions are required to have their counters for receiving payment separate from other counters.

- Conversations at the counters are always recorded. While the main purpose is staff education, the recordings are also used as evidence in case of conflicts. If a visitor wishes to confirm the contents of recordings, he or she must submit an application to the police and present that certificate to NTUC Income, and then they will be allowed to do so (no exceptions). Visitors are presumed to have given their consent, because a warning poster about recording is displayed near the entrance.

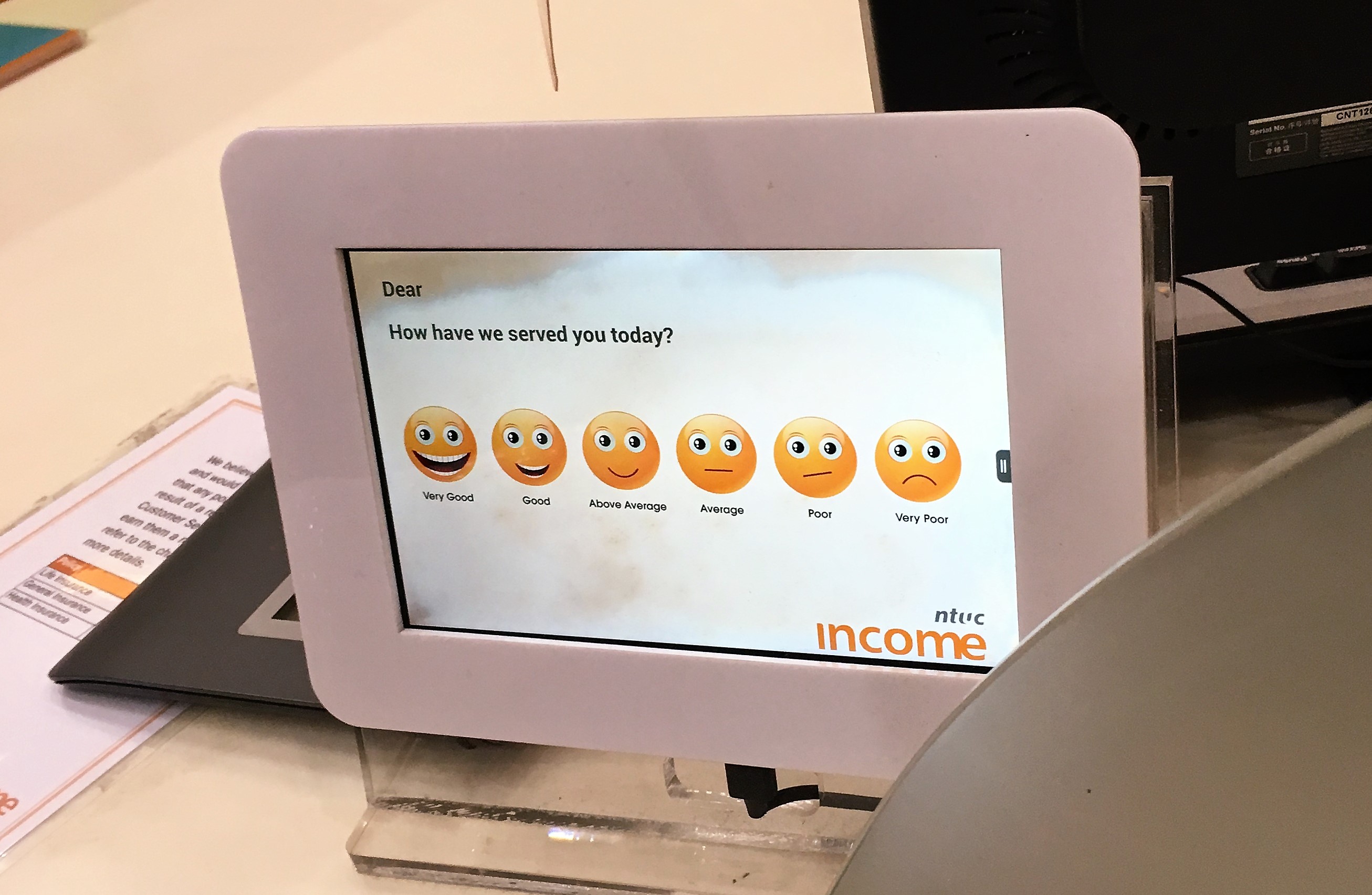

- Each counter has a touch screen for receiving feedback from customers, and customers are asked to evaluate satisfaction with customer service just received on a six-grade scale. While voluntary, about 70% of the customers give their responses, and many choose “5: Good” or “6: Very Good.” The customer’s response is relayed to the employee who served the customer and the Central Back Office in real time. This means that the employee who served the customer can receive feedback while the customer is still right there, allowing the employee to reflect on the service just provided. Furthermore, if the customer gives a “1: Very Poor” or “2: Poor,” then the Branch Manager may talk to the customer about it or listen to the recording.

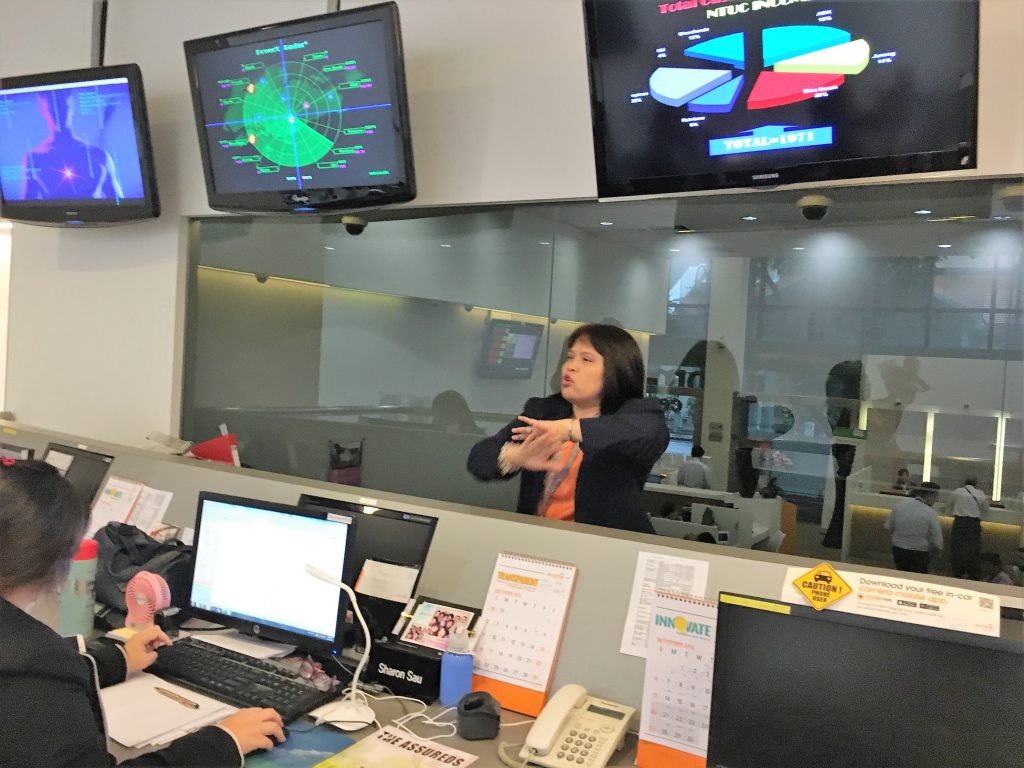

(3) About the Central Back Office

1) Site of the Central Back Office

- Behind the branch at headquarters, there is a Central Back Office that centrally manages information from all branches.

2) Functions

- The following are some examples of the information gathered and managed in real time by applying the central management functions of call centers.

- Images from each branch

- Information about customer service personnel at a branch (name and whether he or she is currently serving a customer, standing by, on break, etc.)

- Number of visitors (purpose of visit and wait time, based on data from the number dispenser machine at the entrance)

- Branch operating rate (operating rate based on the number of visitors, status of customer service personnel at work, and status of visitors waiting)

- Customer satisfaction feedback results

- Two staff members are always on hand to deal with escalation[1] of issues that cannot be handled by the branch, using chat and telephone. Chat is frequently used because it allows the counter employee to conduct escalation using a PC while he or she deals with the customer.

[1] Escalation is a marketing term, often used in call centers. Escalation is often mentioned when an operator facing difficulty dealing with a customer by himself of herself hands over the issue to a senior manager of supervisor. It also includes cases in which the operator seeks instruction from a more senior person.